tl;dr

The tokenisation revolution benefits from three brand-new initiatives.

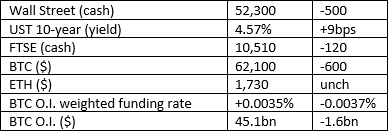

Market Snap

Market Wrap

We now have three consecutive days of inflows to the spot BTC ETFs totalling just over half a billion dollars. If this is the start of a new trend – and that is a very big if – then the final capitulation of this cycle is probably behind us. Which would be good news for us all.

That ignores the Trump issue. He claims the Iran ceasefire is over saying “I don’t want to deal with them anymore”, a sentiment he echoed when he threated to cease trade with Spain – “Spain is a wasted cause … I don’t want anything to do with Spain”. Ho hum.

Curious Cryptos’ Commentary – Securitize (SECZ), Robinhood (HOOD), Ondo Finance (ONDO), and tokenisation

SECZ is a tokenisation platform moving real world assets (RWA) onto blockchains. To date, it is responsible for the tokenisation of $4.4bn of assets sourced from some of the biggest names in the asset management industry, notably BlackRock, VanEck, and BNY Mellon among others.

On July 2nd, SECZ listed on the NYSE via a merger with a SPAC (Special Purpose Acquisition Vehicle), a form of financial transaction which became very popular several years ago. SPACs are empty shell companies that raise funds from equity investors with the purpose of searching out potential acquisitions. Normally priced at $10 a share initially, once the model had been proven successful, the sharks moved in and set up what seemed to be fake SPACs whose only purpose was to enrich the directors and management of the company. That clearly isn’t the case here.

The listing raised $400mm at a valuation of $1.25bn. It quickly traded up to $1.8bn.

What is interesting is that SECZ issued roughly $300mm of SECZ tokens on Solana and Avalanche, making it the largest live tokenised stock globally. As the company put it, “We’re gonna eat our own dog food”, which I must admit is not a phrase I was familiar with before now.

To understand why this is an important development we need to step back a little and look at how stock ownership traditionally works.

In TradFi terms, when you buy a share, it is held on your behalf by a custodian who routes dividends, stocks splits, and other corporate actions into your brokerage account. In legal terms you own a “security entitlement”, a form of ownership which is far more efficient than the old paper share certificate process but is distinctly different from that physical ownership model. It creates many layers of intermediaries including a transfer agent, the depository, the clearing broker, the retail broker, and finally you.

This creates operational and regulatory friction in the form of basis‑point level fees, delays in settlement, slow or error‑prone handling of corporate actions, and capital tied up in margin and collateral buffers across multiple entities. This raises the cost of capital for issuers, lowering productivity, and making us all poorer.

Tokenisation has usually taken the form of assets wrapped for issuance on the blockchain. Legally and operationally, those structures are one step removed from the underlying asset. If we look at the example of BUIDL, BlackRock’s tokenised US treasury fund, the assets are held by a custodian in the exact same way as its traditional funds. No doubt that recording ownership and transfer of assets on the blockchain is far more efficient than the traditional means, but it doesn’t fundamentally change the ownership structure.

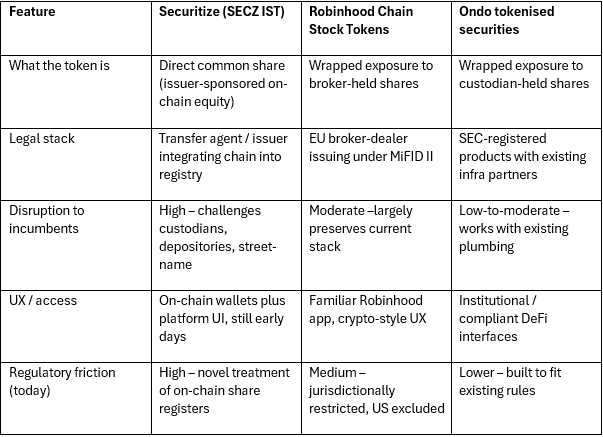

SECZ’s shares on the blockchain are “Issuer-Sponsored Tokens” (IST) for which the onchain token is an actual share of the company, which completely inverts the whole ownership model. The token is the actual share, not a claim on the share. That is a ground-breaking development, fundamentally altering the processes for custody, clearing, the implementation of corporate actions. The concept of “beneficial owner” starts to look like a historical anomaly, a mere staging post on the path from physical shares to a fully decentralised solution.

There is one familiar drawback which is the security issue that applies to owning cryptos in a self-custodial wallet – lose the keys, you lose access to the wallet and the assets held within. That is unpalatable to most investors, and many regulators. It needn’t be quite as drastic as that, for all the KYC and AML checks are still in place when buying the onchain stock. At some point we should expect the regulation to catch up to allow for the cancellation and reissue of stock tokens in a similar way to the cancellation and reissue of paper stocks. However, we are not there yet.

…

On the same day as SECZ’s listing, HOOD announced that its L2 Robinhood Chain had gone live on Arbitrum, an Ethereum L2 with almost instantaneous settlement and fees that amount to fractions of a cent. Share trading will be 24/7, and about time too. In this case the onchain token is a wrapped share, not the actual share itself; each token corresponds to a share held in custody by a US broker-dealer. For now, this initiative does not comply with US securities laws, but it is available in the EU and EEA. Obviously, the UK won’t allow it for there is no desire at the political or regulatory level for doing what is the right thing for investors.

This new model is not so different to current practice, it is a user-experience and market-access upgrade, not a reinvention of the stack.

…

Ondo Finance has been building tokenised versions of stocks and bonds with major asset managers such as BlackRock and Fidelity, though presumably not Vanguard which occupies the rearguard when it comes to blockchain initiatives. Ondo has announced the launch of custodial tokenised US securities operating within the existing regulatory framework – tokenisation built “compliance first”. Again, the tokens are representative of the share, not the actual share itself.

Perplexity very usefully created this table which succinctly summarises the key differences between these three models for trading and ownership of tokenised securities:

Tokenisation is the biggest revolution coming to the financial services industry. We are only at the foothills of tens of trillions of dollars of RWA that will migrate to the blockchain. There won’t be one model, more a range of differing solutions depending upon local regulatory requirements, and investors’ needs and demands.

The biggest obstacle is that the current incumbents in every level of the stack earn significant revenue that is at risk from the tokenisation revolution. They will all try to shore up the regulatory moat with lobbying presented in the form of “investor protection”, but we all know that is a mere façade.