29th June 2026

tl;dr

In response to the BIS’ annual crypto bashing, it’s only fair that the CCC does a bit of BIS bashing.

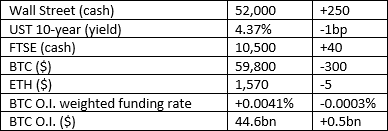

Market Snap

Market Wrap

Trading around $60k has triggered a rush of analysis attempting to answer the question as to whether this crypto winter’s low is in already or not. Don’t believe anyone who claims to know for sure – only hindsight can give us that certainty.

Curious Cryptos’ Commentary – Bank for International Settlements (BIS)

Created in 1930, BIS was the vehicle through which German war reparations were handled. Claiming to be the oldest international financial institution (when you have few, if any, achievements to your name, then barrel-bottom scraping becomes the order of the day), it has extended its remit to “foster international monetary and financial stability”. That could mean almost anything; today the BIS mainly acts as a centre for churning out research that favours the political and financial‑sector status quo. It also has a lucrative sideline providing deposit and investment services for central banks. It surprises me that central banks don’t have that expertise themselves.

Funded by its central bank shareholders, who themselves are funded by the taxpayer, BIS refuses to publish a detailed annual expenditure budget. Transparency and accountability are not concepts widely held to be of value amongst supranational organisations.

Yesterday saw the publication of the BIS Annual Economic Report which is always used for a bit of crypto-bashing. The bureaucrats who inhabit the corridors of irrelevance at BIS HQ in Basel Switzerland are all too painfully aware that blockchain technology is a mortal threat to their own technocratic hegemony and, more importantly, their large tax-free salaries and gold-plated pensions offered in exchange for doing little more than simply turning up at the office, and sometimes not even that. The full report can be found here:

https://www.bis.org/publ/arpdf/ar2026e.pdf

The bit we are interested in is “Chapter III: Anchoring trust in money: innovation beyond stablecoins” The title tells us the conclusion already, but let’s play the game anyway.

…

The core thesis is that stablecoins created on public blockchains, USDC and USDT being the two prime examples, fail “basic tests of money”. Those tests have been defined as singleness, elasticity, and integrity.

Regarding singleness, BIS claims that as stablecoins trade around the peg that this test is failed. Up to a point copper, but with USDC currently priced at $0.9997 this is another glaring example of barrel-bottom scraping. The authors then go on to make the bewildering claim that stablecoins are more akin to ETFs, with no justification.

BIS declares that stablecoins have no elasticity, which itself is defined as having central bank backing. This test is designed to be failed by anything other that fiat and is merely a rhetorical device in a crude attempt to erode trust in stablecoins.

Integrity refers to the potential for illicit use of stablecoins. Claiming that stablecoins fail this test whilst not acknowledging fiat’s and TradFi’s role in facilitating the worldwide drug trade and terrorist financing is so jaw-droppingly biased we now know for certain the authors are having a laugh at our expense.

The first conclusion is one I fully support – strong regulation of stablecoins, but this is hardly ground-breaking. I wonder if the researchers have even heard of the GENIUS Act?

Then there is a bit of fluff about international coordination, presumably extra boxes to be ticked, and more forms to be filled in, with BIS taking on the responsibility justifying an ever-increasing headcount for no discernible benefit for humanity.

Finally, of course, we get the denouement we have all been expecting. There it is: big, black, and monstrous, elephant-size, a great trunk, claws, red eyes. Yes, the report calls for the development and implementation of CBDCs to prevent stablecoins becoming the de facto rails for global money.

…

There is one interesting section that addresses the rising use of USD stablecoins in non-USD economies, which it calls “stablecoin dollarisation”. BIS does not like this for it makes it harder to track cross-border flows when individuals use a smartphone and an on-chain wallet to purchase goods and services.

What BIS totally fails to appreciate is the reason for this growing trend. Today, the diaspora of the world’s poor and dispossessed can lose up to 30% of any money sent back home using traditional payment rails, with weeks of delay, or pay fractions of a cent with instantaneous settlement using stablecoins. This glaring failure by TradFi to address a grievous harm perpetrated on some of the most vulnerable people across the globe doesn’t even raise an eyebrow from anyone at BIS.

But that should not come as a surprise to anyone. The BIS’ main purpose is to ensure its own longevity, and to shore up the moat around TradFi. Such organisations will never have our interests at heart.