tl;dr

The UK surprises us once again in a good way.

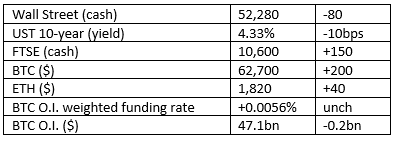

Market Snap

Market Wrap

US CPI landed two days ago at 3.5% compared to estimates at 4.0% and a drop of 0.7% since last month. The change is almost entirely due to fluctuations in the price of oil.

This is instructive on two levels.

Firstly, monthly economic statistics are largely bunkum.

Secondly, risk markets’ responses to numbers like these, to front-run what mandarins in the central bank may or may not do at some indeterminate point in the future, is desperately damaging for productivity and growth.

Two things need to happen. Better data collection and analysis is an absolute prerequisite.

More urgently, removing unelected officials from the process of manipulating the yield curve is so blindingly obvious the right thing to do, it is extraordinary that anyone falls for the myth that central bankers should be involved. Ideally, politicians wouldn’t be consulted either, but I am long enough in the tooth to know the world will never become that sensible.

Anyway, risk markets got an initial boost that has largely reversed on the back of dodgy data, and what that dodgy data might mean for the manipulation of interest rates henceforth.

Curious Cryptos’ Commentary – Cor Blimey, blow me down with a feather, Guv

As we have discussed in recent missives, the UK is taking an increasingly pro-crypto stance, a pivot none of us was expecting. The FCA recently released a regulatory framework for cryptos and detailed rules for stablecoins which have been designed to foster innovation and development. Don’t underestimate the import of this – the UK has long been deliberately antagonistic to the crypto world, regardless of who was stalking the corridors of power at Westminster. The governor of the Bank of England, the hapless and hopeless Andrew Bailey who was previously head of the FCA, lobbied very hard to try to block the stablecoin revolution with overly-prescriptive and deliberately damaging rules, but has been rightly sidelined on that issue now.

The FCA then shocked us again by awarding Coinbase a license under the MiFID rules. My sources indicate that Bailey was particularly aggrieved by that decision.

Now, a 54-strong taskforce that includes all major TradFi banks such as Barclays, J.P. Morgan, Lloyds and so on, has issued a report directly to Bailey, challenging him even further, and piling on more pressure:

The first of two reports, the opening has struck fear into the crypto blockers:

“The aim of this first report is to provide a framework towards how the UK develops a tokenised wholesale financial markets system.”

The reasoning is sound – London remains one of two, maybe three, pre-eminent global centres for financial services. We will very rapidly see the tokenisation of all financial markets which will lead to a step-change in access to those markets, hugely reduced costs for banks and for investors, more refined and focussed risk-management, developments which will benefit us all.

The report quotes an estimate of the amount of real-world assets (RWA) that will be tokenised as $88 TRILLION by 2035. That will surely be an underestimate. But here’s the nub that is getting our fiscally incontinent political masters salivating in an unsavoury manner:

“All of this could translate into a sizeable economic benefit for the UK – an estimated up to £33 billion increase in annual economic output and £14 billion in annual tax revenue by 2035.”

The Treasury has already drafted how it’s going to spend these windfall tax dollars that will keep repeating year after year.

…

The report points specifically to the DIGIT pilot as a starting point for the roadmap.

DIGIT is a project to test the technical details of gilts in a tokenised form – issuance, settlement, trading, and so on. Up to a point this is very welcome, but it is being carried out using HSBC’s private and permissioned in-house ledger known as Orion. Though it uses blockchain technology, as a private platform it is a glorified database. Many of the real advantages of a public blockchain are sacrificed by making it permissioned.

I guess we shouldn’t be too picky at this stage. When DIGIT has been proven to be successful there is no reason it could not be rolled out onto a public blockchain. The pressure to do so will be too great to bear. Indeed, there has been feedback from some industry participants exactly on those lines already. For example, Global Digital Finance argues that “… in the long run, UK digital gilts should be operable across both public and permissioned blockchain networks to maximise distribution, interoperability and secondary‑market depth.”

Can’t argue with that.

…

There is a lot of technical detail and recommendations around those issues, none of which need concern us today. There is one plea that will go unheeded (“A technology neutral approach to tax”) and one very welcome omission – there is no mention of a CBDC.

If this report had been produced by the technocrats in government, it’s only focus would have been how tokenisation can speed up the introduction of a sterling CBDC. No-one in TradFi or the crypto world has the appetite to help the government out on that point.

The report also highlights some specific examples of tokenisation in action today.

As just one example, Baillie Gifford launched a fully tokenised corporate bond fund in June this year on Ethereum and Solana, with a 7% dividend yield. All trading, settlement, and dividend payments take place on the blockchain. Crucially, this initiative is compliant with all current rules and regulations that apply to TradFi.

The direction of travel is very clear. The UK’s financial services industry is being positioned to be a global leader in the race to the total tokenisation of all financial assets. Naysayers should take note and tootle off to do something less damaging elsewhere instead.