26th May 2026 > > BTC DATCOs.

- 2 hours ago

- 4 min read

tl;dr

A brief sojourn into the world of BTC DATCOs.

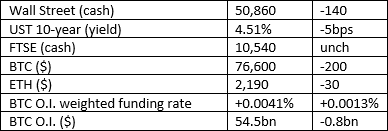

Market Snap

Market Wrap

Resumption of hostilities in the Strait of Hormuz appears to be largely ignored by the markets though the gap in rhetoric, with Trump claiming a deal is almost done and the Iranians denying it, does not inspire a lot of confidence.

Outflows from the spot BTC ETFs last week of $1.3bn is a tremendous disappointment.

Curious Cryptos’ Commentary – BTC DATCOs

10xResearch has issued an excellent analysis of the BTC DATCOs discussing why so many trade at a discount to mNAV (market Net Asset Value) and what might happen in the future. That research is paywalled, and it would be inappropriate to pass on any of the details, but the report does include this table of freely available public information:

The data is in descending order of the discount. If we take the top row, GD Culture Group owns 7,500 BTC (nice!) worth $576mm at the time of writing, whilst the company’s market cap is a mere 7mm putting an effective valuation on each BTC of $935. The last time you could buy BTC that cheap was early 2017, when everyone laughed at me when I confidently predicted a price more than $100k.

I am being very clear (doncha literally hate that phrase?) that making that comment is not a recommendation to buy GD Culture Group, nor any of the others on this list. There are factors at play other than just the amount of BTC on the balance sheet. But one might genuinely expect that within this universe of 27 companies, there will likely be some golden opportunities for those who know how to look for them.

Curious Cryptos’ Commentary – Strategy (MSTR)

It feels wrong to talk about all the other BTC DATCOs without at least some reference to the daddy of them all, MSTR. Chairman Michael Saylor recently surprised everyone by publicly stating that one day MSTR might sell BTC, a sharp change in his previous position. It is worth trying to understand what has changed.

…

The easy part is MSTR’s legacy software business - enterprise analytics/BI software and services that still generates roughly 0.46–0.47 billion USD of annual revenue, with high gross margins and modest growth. Depending on the multiple you apply, probably anything up to 5x, as a stand-alone this business would be worth up to $2.5bn. In the context of a near $60bn market cap for the entirety of MSTR, this is little more than a rounding error though the cashflow is of some use in servicing the liabilities of the preferred stock.

When MSTR initially pivoted to becoming a BTC accumulation vehicle, the playbook was simple. When MSTR stock was trading at a premium to the value of BTC on the balance sheet, stock would be sold to raise cash to buy BTC increasing the amount of BTC per share. In theory, the sensible move would be to sell BTC and buy back MSTR shares when the stock trades at a discount to the value of BTC on the balance sheet, again increasing the amount of BTC per share. The trade is counter-intuitive – MSTR tends to trade at a premium in bull markets, and at a discount in bear markets. This is why Michael famously said he would always be buying the top.

More recently, the company has been selling various forms of preferred shares which carry coupons as high as 11%, though note they are deferrable and non-cumulative. Peter Schiff, long-term arch sceptic of BTC having missed out on life-changing gains by not acting on his own advice to buy BTC when it was trading for a couple of hundred dollars, has described the issuance of these products as a Ponzi scheme. Schiff can’t help but distort the truth to fit his warped view of the world, but in a very narrow sense he has a point. MSTR will continually issue new debt and equity to buy BTC, though some of that cash will be used to pay the dividends as they fall due. Recently the company confirmed it has enough cash to cover two years of dividends. If that is the internal company target, then for every $100 of preferred shares sold, $22 goes into the bank account, and $78 buys BTC, giving an effective leverage of nearly 4x.

Hidden within that playbook is the fact that two years later, there is no cash left to pay the dividend. If cash raised from new preferred shares was used to service those debts, then Schiff’s accusation is on slightly firmer ground, but it isn’t difficult to see how that structure quickly becomes unsustainable.

This is the reason why MSTR will sell small amounts of BTC to retire preferred shares. If you are a crypto-believer, and you think BTC remans hugely undervalued (spoiler alert: it is) this process results in owners of normal stock effectively accumulating BTC at far below the current market price. Not quite as discounted as GD Culture Group, and nor is it an easily calculated price – it depends on the value of BTC when preferred shares are retired. But a discount nonetheless, unless you subscribe to the ECB’s ludicrous claim that “… the fair value of BTC is zero”.

But if you did, I doubt you would countenance reading our near-daily missive.

Comments