tl;dr

A new concept of DeFi might have some far-reaching ramifications.

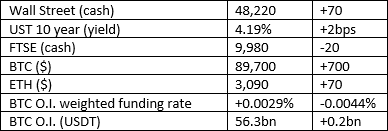

Market Wrap

The first trading day of the year yesterday brought net inflows of a tidy $470mm to the spot BTC ETFs, which is an encouraging start. Let’s hope it’s a portend of the future. If risk appetite for cryptos has returned with the reset of investment and trading books back to zero, it could make for an interesting January.

Curious Crypto’s Commentary – Some intriguing news

Founder of DeFi protocol Curve, Michael Egorov, has released information about a new protocol he is developing which may fundamentally change the way the DeFi works, and which may have a profound impact on a common (mis)conception about BTC.

The maths can be found here, but for anyone who left education behind several decades ago (that includes all the CC research team and I) may struggle to fully understand the maths at work:

https://github.com/yield-basis/yb-paper/blob/master/leveraged-liquidity-paper.pdf

I can do no better than simply quote the abstract at the start of this academic paper:

At the heart of DeFi is the concept of AMMs (Automated Market-Makers). There are many ways to implement AMMs, some more sophisticated than others. In its simplest form a pool consists of two different assets which start with an equal market capitalisation of each asset. As third parties transact with the pool, the pool automatically calculates the exchange rate for each asset that maintains that equal market capitalisation. That is a simple equation to construct and execute, in principle at least.

However, this simple implementation gives rise to what is known as impermanent loss, which should rightly be called – in most scenarios – permanent loss. If you provide both USDC and BTC as liquidity to a pool, and BTC rallies hard (as to be expected), your impermanent loss on your reduced holdings of BTC will likely exceed the trading fees or other incentives you may accrue. This is an undoubted drawback to the basic concept of liquidity pools and AMMs.

Michael, as he sets out clearly in the above abstract, claims he can remove impermanent loss whilst also providing 20% APR on a BTC/USD stablecoin liquidity pool. If he is right, this a gamechanger for DeFi.

A word of warning, Michael is expressly using leverage to achieve this feat of magic. Regular readers know that the CCC is viscerally opposed to the use of leverage in cryptos, in almost all circumstances. The pain taken in the perpetual futures markets by retail investors who think they can play against the big boys who have such a vastly greater access to market knowledge and market flows makes me want to cry sometimes. Just say no to leverage particularly when it is used for perpetual futures.

…

The difference with Michael’s use of leverage compared to products such as perpetual futures, is that though there is a directional investment involved, there isn’t an innate attempt to turbocharge those returns. And neither is there an element of going short. He claims to have back tested for six years, a period which has seen some significant volatility to both the upside and downside. In that time, BTC has ranged from less than $4k to $126k with many significant and sharp drawdowns. If we assume this new product works as it claims to do, every single liquidity pool will move to this new model, fundamentally changing the basic infrastructure of all DeFi protocols.

But there is another equally key point here, which is that there are many who claim that BTC is an unproductive asset. To a certain extent, one can understand why there are those who take such a naïve and negative view. This product destroys that argument for evermore.

As an aside, those who state that BTC is an unproductive asset usually point to Proof-of-Stake coins such as Ethereum and claim that there is an annual yield of around 3% holding and staking ETH.

What utter tosh.

It is true that if you hold and stake ETH, your notional will increase by around 3% per annum. But that is merely inflation in the underlying number of coins. All other things being equal (which they never are) the market capitalisation does not increase simply because there are more coins – the price adjusts downwards to account for the increased supply. If you hold ETH and don’t stake, you are losing 3% per annum, but that is an entirely different proposition from gaining 3% per annum. Note that this analysis is not restricted to ETH but encompasses all coins which pay out rewards that inflate the underlying supply.

I just don’t understand why some people struggle to get their heads around such an obvious and true statement of fact.