30th June 2026

tl;dr

The tokenisation of the repo market is of enormous benefit to the entirety of humankind.

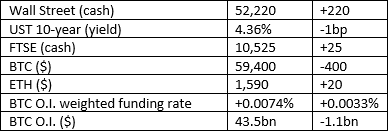

Market Snap

Market Wrap

Crypto prices remain subdued. The last week has seen a very large inflow of BTC to centralised cryptocurrency exchanges from short-term holders who are now significantly under water. Is this the last capitulation? We cannot know until long after the event, but it is most certainly a candidate, potentially paving the way for a recovery.

Curious Cryptos’ Commentary – Repo and AAVE

I must make the point that the CCC does not provide financial advice. Today’s commentary will focus on the functionality being rolled out on Aave V4 to illustrate the impending tokenisation revolution, and how the technology will prevent any possible repeat of the Global Financial Crisis we experienced over a decade ago.

I must also point out that the CC Treasury has long been an investor in AAVE, the coin native to the Aave ecosystem, via secure third-party custody.

…

The repo market is unglamorous, and both misunderstood and under-appreciated within the financial services industry, let alone amongst the public.

A repo trade is simple.

One party to the transaction provides collateral e.g. government bonds and the other party provides cash up to a haircut on the market value of the collateral. Often just one day in length, the repo is closed with the reverse exchange of the collateral and cash plus the interest charged on the loan.

Your mortgage is a variation on this trade, but with a much longer maturity date, and, frankly, extortionate terms that reflect the illiquidity of the collateral, i.e. your house. The cumbersome process of settlement, and the hugely damaging tax known as stamp duty which is one of the most egregious examples of a productivity-destroying tax one could possibly create, makes mortgage rates much higher than they could otherwise be.

The repo market is often referred to as the “plumbing” of the banking industry. It allows the rapid movement of cash from banks that have a short-term excess to those that have a short-term deficit. Without it, there is no banking industry with all the attendant fateful consequences, an observation to which we shall very shortly return.

It is estimated that every day over $3 TRILLION of cash changes hands via the repo market. Though increasingly executed via electronic trading, thus simplifying the booking and reconciliation of trades, there are vast armies of back-office staff required to monitor and measure each individual bank’s cash position and exposure to both the collateral and each individual counterparty.

And that latter point is crucial.

The Global Financial Crisis, a direct result of some of the most poorly-designed financial regulation ever imagined, was precipitated by a crisis of confidence between banks. If the party providing cash for the repo trade becomes concerned that its counterparty will not be able to return the cash the next day, then no amount of collateral – in a stress situation – can possibly compensate for that risk. Once all banks start thinking that about all other banks, the repo market grinds to a halt. Banks start hoarding cash where they can, those that can’t must get an instantaneous bailout from the government, and no credit facilities will be available to business or individuals.

We came very close to a catastrophic breakdown in the global financial system. If that had happened, we would still be suffering serious side effects even today. The reason it didn’t is that central banks reverted to their one true task as lender of last resort. Hats off – they did that job to perfection. It’s a shame they didn’t continue to restrict themselves to that one responsibility since then.

There are other issues with the current TradFi solution to managing cash flow for banks. There are many settlement issues to resolve every day, not helped by T+1 settlement in the US and T+2 in Europe. There can be layers of intermediaries, all taking a fee from the process.

Any reduction in the productivity of banks feeds directly into the cost of capital for all business, which in turn reduces the productivity of business, lowering growth, putting upward pressure on inflation metrics, lowering tax revenues, and generally making us all poorer in the process. There is a moral imperative to reducing the costs and burdens placed on banks, including the deliberate targeting of banks by successive and increasingly ill-informed governments of all hues.

…

Founder and CEO of Aave, Stani Kulechov has written a guide to Aave V4 which is designed to bring the repo market on-chain:

https://x.com/StaniKulechov/status/2067993849306263706

Stani breaks the repo market down into three separate categories – securities backed lending, repo, and securities lending. They are all essentially the same though with different timescales and different investors. For our purposes we lump them all together.

Stani explains the liquidity and market structure provided by Aave V4, which need not detain us here, though I do highly recommend you acquaint yourselves with the detail.

What is important is the benefits that tokenising the repo market will bring to everyone.

From an operational perspective there is instantaneous settlement with total transparency on the blockchain. No more waiting around for cash, and no reconciliation or settlement issues ever again. That is a whole heap of expensive and now redundant back-office jobs removed in a flash lowering the cost of capital for non-financial business. The markets will be 24/7, which is a key requirement for all financial services soon.

Risk isolation becomes total, compliance and regulatory monitoring become a trivial task, again dramatically reducing the headcount required for risk management and compliance teams. Layers of intermediaries, who generally add no value to anything, are disintermediated at a stroke. Everyone’s counterparty becomes a single entity, in similar fashion to the role clearing houses play in swaps and derivatives markets. This simplifies and centralises issues around KYC, national and international rules and regulations, and helps ensure for regulated participants there is no regulatory risk. For private investors, access to the repo market for your retail sized holdings becomes a real possibility, giving you a new and lucrative income stream that is currently denied to you. That has the additional benefit of annoying senior executives at TradFi banks.

Oh, and maybe the greatest gift is that there can never be a repeat of the Global Financial Crisis. A centralised counterparty and the pre-programmed return of cash via a smart-contract repo totally removes counterparty risk.

Even the UK regulator can see the sense in that.